Sea fisheries

Scotland - Contribution to the Economy

Employment

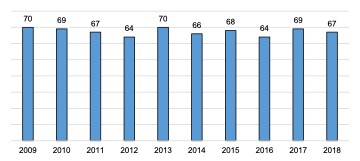

Sea fisheries employment has been on a downward trend over the last decade, with a 25% reduction since 2014 and a 44% reduction since 2009, see figure below, ‘Scottish Solway: Employment, 2009 – 2018′.

Scottish Solway: Employment, 2009 – 2018. (Source: Office for National Statistics (Various) (BRES))

It is worth noting that this data is from the official source of the Business Register and Employment Survey (BRES), however it is understood that the region has many more fishermen than displayed through this data. It may be that some fishermen are employed elsewhere or other factors mean they are not included in this data.

The number of fishers working on Scottish Registered vessels in Dumfries and Galloway is 274 according to the Scottish Sea Fisheries Statistics 2018. However, the comparison of BRES employment numbers to Scottish Sea Fisheries Statistics recording of fishers working on Scottish registered vessels has disparity for other areas as well. For example these numbers are 100 in BRES compared to 291 for 2018 respectively in Orkney. This data refers to ‘fishers’ not specifically those employed in Dumfries and Galloway, so the perception of employed fishermen is much higher than those officially recorded by BRES as in employment in SIC 0311 in Dumfries and Galloway.

Location Quotients (LQ) provide information on the representation of marine industry sectors in Dumfries & Galloway in comparison with Scotland. The LQ compares the industry’s share of regional employment with its share of national employment – an LQ greater than one indicates a greater concentration of sector employment than Scotland as a whole, whilst an LQ lower than one indicates a lesser concentration.

The LQ of the fishing industry in Dumfries & Galloway has declined over time as employment has declined, in parallel employment in Scotland has increased (+38% since 2009), see figure below, ‘Scottish Solway: Sea Fisheries Location Quotients, 2009 – 2018’.

What this means is that sea fisheries significance as an employer (relative to Scotland) has decreased. Nevertheless, that is not to say that its importance as a sector and employer has decreased – it is often the ‘backbone’ and supports the livelihood of local residents in many small rural communities within the Solway.

Scottish Solway: Sea Fisheries Location Quotients, 2009 – 2018. (Source: Office for National Statistics (Various) (BRES))

Economic Output – Turnover and GVA

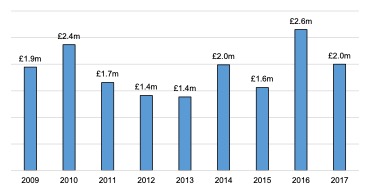

Both turnover and GVA have been relatively flat with a peak in 2016 due to a spike in the value of the catch (as discussed below). This trend may seem odd given the fall in the level of employment, but this is reflective of increase in the price of fish, and therefore increased turnover and profitability. The notable increase in 2016 was driven by a 15% increase in the average price of Scallops, from £2,098 per tonne to £2,411 per tonne (Marine Scotland, 2017b). See Figures below, ‘Scottish Solway: Sea Fisheries Turnover, 2009 – 2017’ and ‘Scottish Solway: Sea Fisheries GVA, 2009 – 2017’.

Scottish Solway: Sea Fisheries Turnover, 2009 – 2017. (Source: Scottish Government (2019) (SABS))

Scottish Solway: Sea Fisheries GVA, 2009 – 2017. (Source: Scottish Government (2019) (SABS))

The GVA to turnover ratio provides an insight into the relative levels of productivity with the sector. The ratio declined from 2011, likely as a result of cost pressures on the industry such as increased fuel costs. However, productivity has increased from 2015 onwards, likely due to a) the decline in employment (reduced costs) and b) the increase in value of the catch over this period (increase in price), see figure below, ‘Scottish Solway: Sea Fisheries GVA to Turnover Ratio, 2009 – 2017’.

Scottish Solway: Sea Fisheries GVA to Turnover Ratio, 2009 – 2017. (Source: Scottish Government (2019) (SABS))

The table below, ‘Scottish Solway: Tonnage Landed by Selected Species, 2009 – 2018’, shows the landings of the main species of shellfish and total landings. Data for individual demersal and pelagic species are not shown due to data suppression. A total of 2,416 tonnes of sea fish and shellfish was landed in 2018. Almost the entire catch (99.6%) was shellfish, with queen scallops and scallops by far the most important species, accounting for 49% and 34% of total landings, respectively. There has been a large decline in the tonnage of landings in recent years, with a -50% decline since 2014, and a -76% decline since the 2011 peak. Consultees reported that this is largely due to increased competition over the scallop grounds in the Irish Sea, particularly with the Isle of Man, and a general decline in scallop stocks. This has forced much of the Scottish Solway scallop fleet to fish outwith the Irish Sea, primarily in the English Channel.

| Scottish Solway: Tonnage Landed by Selected Species, 2009 – 2018 |

|

2009

|

2010

|

2011

|

2012

|

2013

|

2014

|

2015

|

2016

|

2017

|

2018

|

Change since 2014

|

% change since 2014

|

|

Queen

Scallops

|

3,713

|

6,741

|

8,859

|

7,019

|

5,252

|

3,034

|

3,343

|

2,542

|

1,541

|

1,173

|

-1,860

|

-61%

|

|

Scallops

|

1,382

|

1,522

|

1,216

|

1,170

|

1,020

|

1,371

|

856

|

1,404

|

822

|

831

|

-540

|

-39%

|

|

Whelks

|

106

|

119

|

110

|

140

|

193

|

263

|

241

|

300

|

336

|

307

|

+44

|

+17%

|

|

Razor Clam

|

30

|

0

|

4

|

65

|

146

|

88

|

169

|

251

|

174

|

40

|

-48

|

-54%

|

|

Lobsters

|

47

|

62

|

51

|

46

|

43

|

40

|

50

|

62

|

45

|

39

|

-1

|

-4%

|

|

Crabs

|

11

|

8

|

7

|

6

|

5

|

4

|

4

|

4

|

5

|

21

|

+18

|

+466%

|

|

Nephrops

|

45

|

52

|

18

|

4

|

18

|

18

|

20

|

18

|

15

|

3

|

-15

|

-84%

|

|

Shellfish

Total

|

5,341

|

8,846

|

10,265

|

8,450

|

6,678

|

4,817

|

4,683

|

4,582

|

2,937

|

2,415

|

-2,402

|

-50%

|

|

Demersal

Total

|

3

|

9

|

2

|

2

|

3

|

3

|

1

|

2

|

4

|

1

|

-2

|

-75%

|

|

Pelagic

Total

|

2

|

1

|

1

|

1

|

3

|

2

|

1

|

0

|

0

|

0

|

-2

|

-87%

|

|

Total

|

5,346

|

8,857

|

10,267

|

8,453

|

6,684

|

4,823

|

4,686

|

4,584

|

2,941

|

2,416

|

-2,407

|

-50%

|

Source: Marine Scotland (n.d.).

The table below, ‘Scottish Solway: Value Landed by Species, 2009 – 2018’, shows the value of landings of the main species of shellfish and total landings. Despite the -50% fall in the total catch (tonnage) since 2014, the total value of the catch has increased by +4% within the same period, indicating a strong rise in the price of shellfish. As noted above, between 2015 and 2016, the average price per tonne for Scallops increased by +15% over the course of one year (driven by an increase in demand and decline in the supply).

| Scottish Solway: Value Landed by Species, 2009 – 2018 |

|

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

Change since 2014 |

% Change since 2014 |

| Scallops |

£2.7m |

£2.6m |

£2.4m |

£2.3m |

£2m |

£2.7m |

£1.9m |

£3.7m |

£2.4m |

£2.5m |

-£206k |

-8% |

| Queen Scallops |

£1.6m |

£2.6m |

£3.6m |

£2.9m |

£3m |

£1.4m |

£1.9m |

£2.1m |

£1.9m |

£1.5m |

+£94k |

+7% |

| Lobsters |

£506k |

£649k |

£546k |

£495k |

£434k |

£404k |

£504k |

£717k |

£624k |

£584k |

+£179k |

+44% |

| Whelks |

£58k |

£61k |

£63k |

£84k |

£127k |

£215k |

£195k |

£287k |

£367k |

£361k |

+£146k |

+68% |

| Razor Clam |

£82k |

£* |

£14k |

£196k |

£452k |

£331k |

£771k |

£1.2m |

£1.1m |

£324k |

-£10k |

-2% |

| Crabs |

£12k |

£* |

£* |

£* |

£* |

£* |

£* |

£* |

£* |

£62k |

+£57k |

+1,357% |

| Nephrops |

£95k |

£98k |

£39k |

£* |

£38k |

£43k |

£38k |

£42k |

£34k |

£* |

-£34k |

-79% |

| Shellfish Total |

£5.1m |

£6.4m |

£6.6m |

£6m |

£6.1m |

£5.1m |

£5.3m |

£8.1m |

£6.2m |

£5.4m |

+£230k |

+4% |

| Demersal Total |

£12k |

£19k |

£* |

£* |

£16k |

£16k |

£* |

£* |

£34k |

£* |

– |

n/a |

| Pelagic Total |

£* |

£* |

£* |

£* |

£* |

£* |

£* |

£* |

£* |

£* |

– |

n/a |

| Total |

£5.1m |

£6.4m |

£6.6m |

£6m |

£6.1m |

£5.1m |

£5.3m |

£8.1m |

£6.2m |

£5.4m |

+£218k |

+4% |

Source: Marine Scotland (n.d.). Note: Values below £10,000 are suppressed

Across Scotland, overall landings were down -6% from 2014. Despite this decline in landings, values rose by 16% due to the rising price of fish. Shellfish has seen a -16% decline in landings since 2014 and 9% increase in catch value (Marine Scotland, 2019). See figures below, ‘Tonnage: Scottish Solway as a % of Scotland, 2009 – 2018’ and ‘Value: Scottish Solway as a % of Scotland, 2009 – 2018’.

As a percentage of the total landings, the Scottish Solway is a fairly minor contributor to the Scottish fishing industry, accounting for 0.9% of the tonnage and 1.3% of the value in 2018. However, in terms of individual species, Dumfries & Galloway accounted for 96% of queen scallops, 12% of scallops and 21% of whelks landed in Scotland (by weight).

Kirkcudbright is the largest scallop landing port by tonnage and the second largest by value in Scotland. However, it should be noted that Kirkcudbright’s scallop fleet is ‘nomadic’, meaning that it does not necessarily fish in the Solway Firth (or the Irish Sea to the west). The Kirkcudbright fishing fleet is primarily active in the English Channel with some activity in the Irish Sea, and are known to fish up the North East coast of Scotland, although landings still take place in Kirkcudbright. Interestingly, mainly boats registered on the Isle of Man fish in the Solway Firth.

Tonnage: Scottish Solway as a % of Scotland, 2009 – 2018. (Source: Marine Scotland, n.d.)

Value: Scottish Solway as a % of Scotland, 2009 – 2018. (Source: Marine Scotland, n.d.)

In 2018, the level of all fish and shellfish exports from Scotland were down -6% on the previous year and -19% since 2014. Further, the percentage of total production exported was down five percentage points since 2014.

There is limited data available for the export of fish (dUnited Nations Commodity Trade Statistics Database), and only for commercial fishing and aquaculture (combined) at the Scottish level. See table below, ‘Fish and Shellfish Exports (Tonnes) Scotland, 2014 – 2018’. It is likely that this data understates the amount of Scottish fish that is exported, as a proportion of Scottish fish production is used as an input by English based fish processors which is the exported, and is therefore classified as an export from England.

| Fish and Shellfish Exports (Tonnes) Scotland, 2014 – 2018 |

|

Total Production

|

Tonnage Exported

|

% Exported

|

|

2014

|

479,360

|

219,176

|

46%

|

|

2015

|

439,016

|

175,008

|

40%

|

|

2016

|

453,278

|

186,981

|

41%

|

|

2017

|

474,141

|

188,732

|

40%

|

|

2018

|

439,431

|

178,050

|

41%

|

Source: Marine Scotland (n.d.), HMRC

Note: Combined commercial fishing and aquaculture

It is difficult to estimate the tonnage of shellfish exported from the Dumfries & Galloway from these figures. However, around 70% of the total UK scallop catch is exported (Cappell et al, 2013) and consultation evidence also indicated that a large proportion of Scallops production is exported, primarily to France.

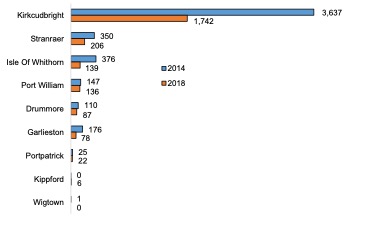

The map below presents a breakdown of the main landing ports in Dumfries & Galloway, with Kirkcudbright being by far the biggest and accounting for 72% of landings by tonnage.

Main Landing Port in Scottish Solway, 2018. (Source: Marine Scotland, n.d.)

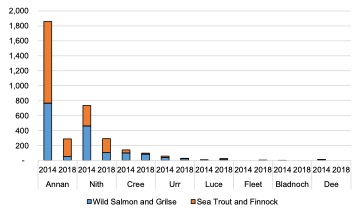

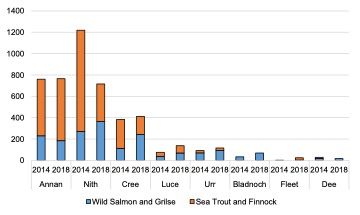

The figures below, ‘Scottish Solway: Landing weight (Tonnes) by Landing Port’ and ‘Scottish Solway: Landing Value by Landing Port’, show the change in catch weight and value since 2014 by landing port. Overall, reflecting trends across the sector the catch was considerably down in the largest ports, with tonnage reductions of -52% in Kirkcudbright, -41% in Stranraer and -63% in Isle of Whithorn. By contrast, the value of catch in the major ports has increased by +9% in Kirkcudbright, +28% in Stranraer and +5% in Isle of Whithorn, again highlighting that increased prices (in particular, shellfish) have offset the decline in the weight (tonnage) landed.

Scottish Solway: Landings Weight (Tonnes) by Landing Port. (Source: Marine Scotland, n.d.)

Scottish Solway: Landing Value by Landing Port. (Source: Marine Scotland, n.d.)